Opinions: £10,000 when you turn 25?

Wouldn’t it be nice if, on your 25th birthday, you woke up to £10,000? This is the proposal with which thinktank, Resolution Foundation, has been grabbing headlines with this week.

Any sort of policy that involves handouts is bound to cause controversy, and though at this point it’s just a suggestion, this one’s no different. The Daily Mail have unsurprisingly branded the so-called Citizen’s Inheritance a “free nest-egg”, while Chloe Westley of the TaxPayers' Alliance calls it a “one-off cash bribe”.

But there have been supporters of the idea, too. Olivia Utley of Reaction says that since millennials have been guinea pigs for tuition fees and soaring house prices, they’ve earnt the right to have something good trialled on them too. The Times too, agrees that the 'looming crisis of trust between old and young' has become so urgent that radical proposals are desperately needed.

And the UK population? What do they think? Are the taxpayers who would fund these grants incensed? Do the 25-year-olds who would be receiving them feel they’re needed?

We gathered views of young and old alike to investigate how tough life really is for millennials, and how willing the rest of the population is to help them.

The Perennial Millennial Struggle

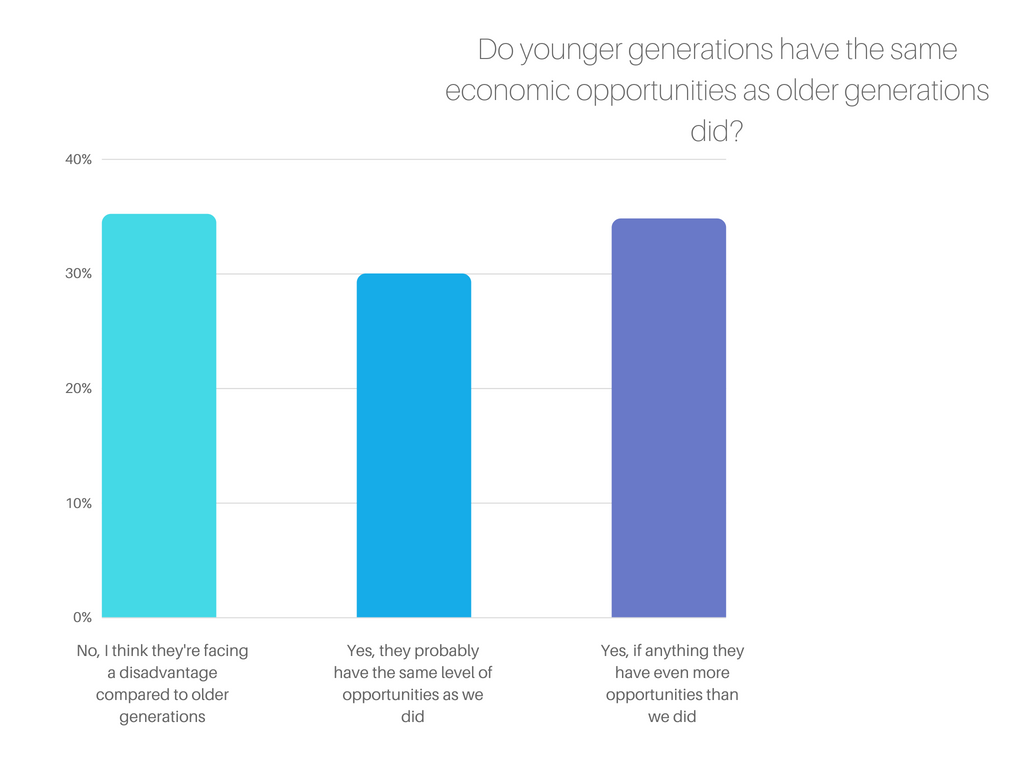

It’s common knowledge that millennials haven’t come of age in the friendliest of economic climates.

Home ownership rates have almost halved: only 33% of millennials will own a home by the time they’re 30, a figure that was at 60% in the heyday of baby boomers. Because, while house prices leapt 259% between 1997 and 2016, earnings only rose by 68%.

More people now are going to university than ever (an estimated 49% of the population went in 2016, but it’s not necessarily financially beneficial. While three years at university now brings with it £30,000 plus of student debt, for one in ten universities, graduate earnings are lower than those of non-graduates.

In these times of student debt, expensive rents and lower incomes, how do 18-35 year olds feel about their day-to-day spending?

Even amongst over-35s, there is an understanding that it’s harder now, or at least no easier than it was, to afford the costs of living. Over 35% of the older generations admit that life’s financially more difficult now and a further 30% think it’s probably the same.

Times are tough, it seems. It’s a trend that explains the success of challenger brands like Monzo, whose fee-free banking is heavily targeted at millennials precisely because it helps people stay within their means.

Of course, budgeting responsibly is a necessary part of life. But is it one that should land squarely with individuals? Or are there other bodies who ought to be helping to ease the financial burden?

Young people are less entitled than mass-media often paints them, with over a third deciding that they alone are responsible for affording the necessities. However, almost half acknowledge that the government should also assist, perhaps with schemes exactly like the £10,000 citizen’s inheritance.

There is also a healthy contingent who feel that brands themselves ought to price their products reasonably.

Many brands have picked up on the financial difficulties of young people. From 16-25 railcards (soon to be raised to 16-30) to theatre tickets banded into price brackets escalating with age. From discounted software and streaming service subscriptions, to NUS cards being accepted in high street shops and supermarkets. There is a lot to be said for attracting young consumers with inviting prices.

Once reduced prices have encouraged millennials to part with their in-demand cash, they may even become life-long customers of the brand they’re choosing to spend with.

Over 40% of young people are keen to stay brand-loyal even after the student discount season has ended. Perhaps, then, these cash-strapped millennials are an opportunity: by pricing kindly to the young, brands can retain them as customers once their careers pick up and they’re more carefree with their wallets.

Support from previous generations?

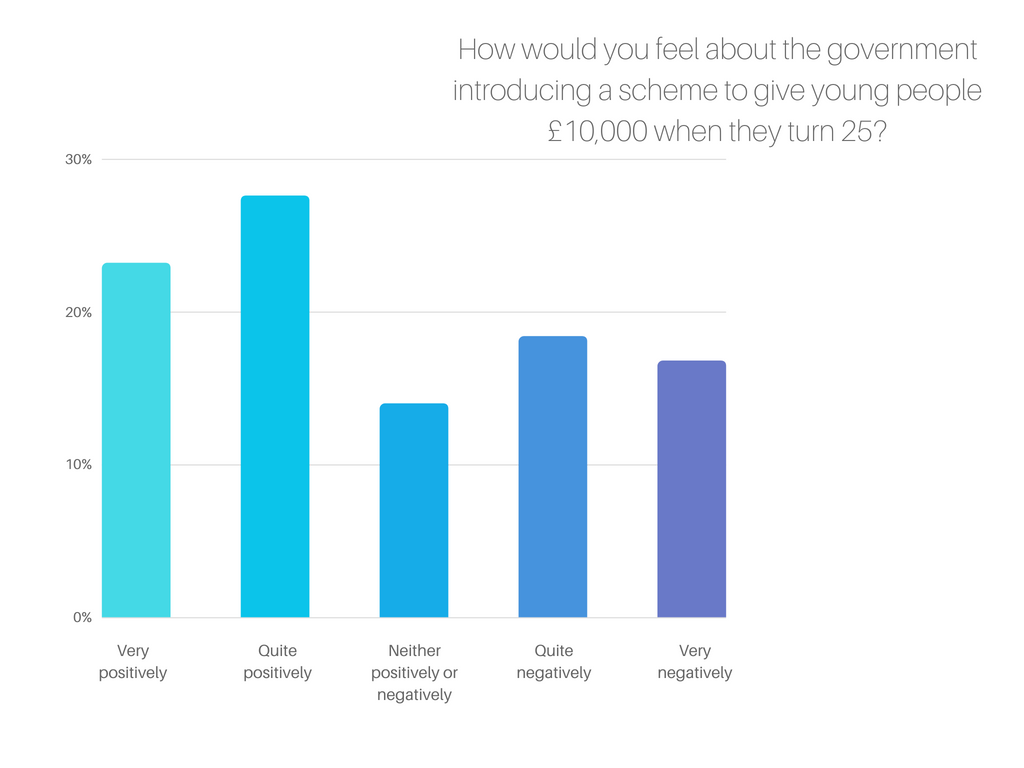

How does this all sit with the over-35s? Outrage from many (older) journalists over the proposed Citizen’s Inheritance gives the impression that older people are rather cross. A blanket donation to an entire generation, regardless of family wealth or job title, does indeed pose issues. After all, it’s not only younger generations who are under financial pressures.

But the reaction from the UK public told a more compassionate story than the one the press are putting out. On the whole, it seems that older generations view the scheme favourably.

Over half feel positively about the idea, with a further 18.4% reacting neutrally. Does this generosity extend to the idea of companies subsidising young people’s purchases as well?

Again, opinion paints a giving picture. 48% are positive about brands reducing young people’s prices, and 31.6% feel neutrally. This is particularly impressive given the results aren’t dramatically different when asked how they would feel about these same benefits being applied to their own age group, or an age group they are yet to come into.

With desire for change comes opportunity

These results blend naturally: young people are finding it difficult to keep up with financial duties; older people are supportive of ways to ease these burdens. Whether or not a proposal as radical (and one that’s not means-tested) as the Citizen’s Inheritance becomes a reality, there is a firm desire to nurse the financial inequalities between generations, from both sides of the fence.

Companies, then, have an opportunity to get involved where the government might not. Since offering reduced prices for younger generations doesn’t elicit bad blood with those who’ve already outgrown these benefits, it seems like a win win scenario.

Not only will it help make life more affordable for millennials and generation Z - people who otherwise probably wouldn’t stray far from cheap own-brands - but it gives brands a way to ingratiate themselves with the consumers of the future. Win them over with attractive prices while they’re not so well-off that they can be picky, and companies may well keep their loyalty even as they grow older, and the prices grow with them.

To see the results in full, if you’d like to test a new pricing plan, or quiz consumers on how much they’d be willing to pay for your product or service, get in touch with Attest today.

Want more like this?

Want more like this?

Insight delivered to your inbox

Keep up to date with our free email. Hand picked whitepapers and posts from our blog, as well as exclusive videos and webinar invitations keep our Users one step ahead.

By clicking 'SIGN UP', you agree to our Terms of Use and Privacy Policy

By clicking 'SIGN UP', you agree to our Terms of Use and Privacy Policy

Other content you may be interested in

Want more like this?

Want more like this?

Insight delivered to your inbox

Keep up to date with our free email. Hand picked whitepapers and posts from our blog, as well as exclusive videos and webinar invitations keep our Users one step ahead.

By clicking 'SIGN UP', you agree to our Terms of Use and Privacy Policy